Here is an email I recently received.

Note that I live in Maryland, USA and not Ontario, Canada.

Chem-Dry, the world's largest and highest rated carpet and upholstery cleaning franchise system with 3,500 units in 35 countries, has recently opened new territories and will be exhibiting and recruiting new franchisees at the show.

The show is being held at THE INTERNATIONAL CENTRE in Mississauga, Ontario on September 7th and 8th. ChemDry has been ranked the #1 carpet cleaning franchise by Entrepreneur magazine for 25 consecutive years.

With our proprietary hot carbonating extraction cleaning process and ongoing marketing and operational support, ChemDry is a franchisor that helps you grow.

We offer in-house financing with as little as $9,995 down and total investment starting at $41,000.We also deliver top-line results.

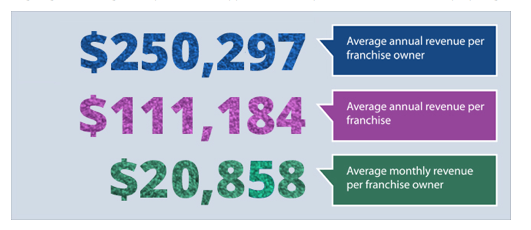

Check out our average franchise sales numbers:

Usually, I would simply look up the franchisor's FDD and compare this earning's claim with the Item 19 claim.

But, this is a much more difficult case. I don't know much about the Ontario Franchise Disclosure law - except Webster tells me it that it is for lawyers and not franchise investors.

So, I looked up the Item 19 for Chem-Dry in the US, How Much Can I Make.

First, the Item 19 is not based on the franchise owner's reported profit and loss statements.

"HRI does not currently require all Chem-Dry business franchise owners to provide periodic revenue and other financial reports concerning their franchises.

In February, 2013, HRI conducted a system-wide survey requesting that all franchise owners provide certain financial and other information relating to the operation of their Chem-Dry business franchises during 2012.

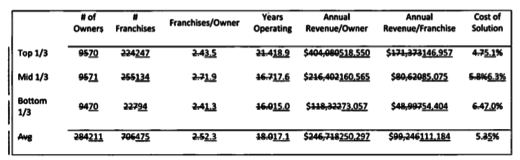

As of December 31,2012. HRI had 1,081 franchise owners who operated 2,039 Chem-Dry business franchises.

Of those, 211 franchise owners (the "Responding Franchise Owners"), who collectively own 475 Chem-Dry business franchises, and who have owned their businesses at least 2 years, provided complete 2012 financial information in response to the survey and operated those franchises throughout all of 2012."

Second, and it gets more tangled, here is the chart from the survey, click on it to expand it.

The average revenue number reported from the US survey as representative to Ontario prospects is the same: $111,184!

It is it all all plausible that the 211 franchisees who completed the Chem-Dry survey in 2012 forms a reasonable basis to tell a prospect in Ontario what he or she might make?

Perhaps some franchise attorney in Ontario can tell me?

For the 5 Most Fascinating Stories in Franchising, a weekly report, click here & sign up.