It's not much of a useful analytical piece. The piece did not move the market, the Bloomberg editorial standard. Deep analytics must not sell anymore in our time-starved span of attention. The piece is Wall Street personality and issue focused.

Franchised Restaurant companies require a lot more investor due diligence, on both the equity and bond investor side, and on the franchisee side. And I want to talk about that.

First, franchisors don't release their franchisee financials results other than same store sales. 100% franchisors like DineEquity (NYSE:DIN), Burger King and Tim Hortons (NYSE:THI) don't release a single franchise operations number.

Popeyes (NASDAQ:PLKI) alone of the publicly traded group releases franchisee EBITDAR - EBITDA less rent.

Some limited clues may be possible from the 10Q/10K statements and the franchisors' Franchise Disclosure Document that details unit opens/closes.

The 10Qs/10Ks don't detail why units open or close, but the FDD broadly classifies closings into categories.

The same store sales metric is more visible.

But to focus in isolation as Businessweek tried (Burger King's same store sales exceeded McDonald's) is flawed: a .5% same store sales gain on a $2.7 million sales base yields a much more healthy picture than 2.0% on $1.0M store AUV base.

Actually, both comps and unit opens/closings need to be examined together, it's very possible to open a lot of stores but realize negative same store sales trends (Five Guys, Smashburger are best recent examples, experiencing both conditions).

Positive same store sales are nice, but are they profitable sales (might not be if discounting is involved) and are they high enough (restaurants need about 2% growth per year typically to cover inflation).

Bad debt expense, the value of franchise royalties not paid to the franchisor and eventually aged and reported, is also a poor, lagging metric. Once bad debt expense is posted, it's really late in the business cycle, the franchise model problem is very intense, the horse is out of the barn.

Franchisees don't talk much - they are afraid to and told not to, and are constrained from communicating via franchise agreements. More research and due diligence is needed. Consider the 3G Capital and Fortress experience, their astoundingly bad 2012 Quiznos investment ($350 million investor group loss and counting).

Getting franchisee EBITDA is great (it is possible, but you have to dig and hire the right people) but it's only half of the story. Restaurants are capital expenditure (CAPEX) intense and some measure of after tax, after debt service, after loan amortization economic gain or loss number is needed.

As usual, business analysis is not what you read on the cuff - it's not what you expect, it's what you inspect.

For the 5 Most Fascinating Stories in Franchising, a weekly report, click here & sign up.

Ever wondered how much it costs to own a McDonald's franchise. If you are interested, here are the details... direct from the McDonald's site:

Acquiring a Franchise

Most Owner/Operators enter the System by purchasing an existing restaurant, either from McDonald's or from a McDonald's Owner/Operator. A small number of new operators enter the System by purchasing a new restaurant.

The financial requirements vary depending on the method of acquisition.

Financial Requirements/Down Payment

An initial down payment is required when you purchase a new restaurant (40% of the total cost) or an existing restaurant (25% of the total cost). The down payment must come from non-borrowed personal resources, which include cash on hand; securities, bonds, and debentures; vested profit sharing (net of taxes); and business or real estate equity, exclusive of your personal residence.

Since the total cost varies from restaurant to restaurant, the minimum amount for a down payment will vary. Generally, we require a minimum of $750,000 of non-borrowed personal resources to consider you for a franchise. Individuals with additional funds may be better prepared for additional or multi-restaurant opportunities.

Financing

We require that the buyer pay a minimum of 25% cash as a down payment toward the purchase of a restaurant. The remaining balance of the purchase price may be financed for a period of no more than seven years. While McDonald's does not offer financing, McDonald's Owner/Operators enjoy the benefits of our established relationships with many national lending institutions. We believe our Owner/Operators enjoy the lowest lending rates in the industry.

Ongoing Fees

During the term of the franchise, you pay McDonald's the following fees:

Service fee: a monthly fee based upon the restaurant's sales performance (currently a service fee of 4.0% of monthly sales).

Rent: a monthly base rent or percentage rent that is a percentage of monthly sales.

Restaurants were said today to be a leading indicator of investment market power in 2015.

Five recognizable realities exist in the space that are both challenges and addressable opportunities.

Insufficient restaurant profit flow through rates, M&A upside and downside, dysfunctional early IPO valuations, franchisor overfishing and CAPEX measurement are issues.

The restaurant space slogged it out in 2014.

Finally, with meaningful wisps of economic recovery seen in Q4 and more disposable income running in the system, hope of discretionary spending is seen.

Several attractive IPOs, Habit (NASDAQ:HABT), and Zoe's (NYSE:ZOES) made it through the gauntlet and with more to come in 2015 (SHAK and others).

On January 5, Jim Cramer of CNBC said that domestic restaurants are key to the market performance in 2015. That sets a high bar.

Of course a reality gap exists between Wall Street wants and needs and Main Street corporate realities. The prism restaurants operate is not really seen by Mr. Market. Looking beyond the veil, restaurants are a tough business, talk to the departed CEOs of Darden (NYSE:DRI) and Bob Evan's (NASDAQ:BOBE) about that

There are several ongoing dynamic restaurant financial realities that underpin restaurant performance.

All are realities.

All are opportunities.

And, all can be fixed & are addressable.

1. Need to manage and improve restaurant profit flow through. Also known as PV ratios, we should not have been surprised to hear that the ten year US McDonald's (NYSE:MCD) average sales per unit (AUV) grew $770,000 but flow through grew by just $70,000, or 9%. Was it all those beverages that cannibalized food? A national survey just reported the McDonald's average consumer expenditure reported at $3.88 per person, which is shockingly low.

It's a broader restaurant issue however: For a client, I recently examined three QSR brands [McDonald's, Burger King (NYSE:QSR), Wendy's (NASDAQ:WEN)] and three casual dining brands [Denny's (NASDAQ:DENN), Bob Evans and Applebee' (NYSE:DIN)] that grew average store sales only $46,000 and unit EBITDAR by only $500 between 2009 and 2014, about a 2% flow through rate. Shockingly low sales gains, even worse flow through.

Both Chili's (NYSE:EAT) and Outback (NASDAQ:BLMN) added a boatload of new menu items at or under $10 to their menus in 2014, and Chili's added their signature fajitas to its 2 for $20 menu. This exasperates the flow through problem; let's hope additional upsell initiatives kick in to maintain the average check.

This is the result of hyper food inflation, and some labor cost inflation and a lot of discounting. The fix? Multi dimensions required. Start by not listening to the ad agencies to take the fast, cheapo way out and simply discount; get staff to upsell.

2. M&A is both a value enhancer and a destructor: Both good and bad M&A are in the background and the foreground. Bad M&A can be seen considering Darden and Bob Evans this year. Good: future possible spinoff BEF foods for $400M ($413 million value estimate by Miller Tabak). Its current EBITDA baseline is only a few million dollars. Spin it and give the money to shareholders.

Bad M&A: waiting so long to dump both Red Lobster and Mimi's . Interestingly, financial disclosure and visibility of both brands by their HOLDCOs was awful. Who really knew before Darden spilled the beans in 2014 that weekly customer counts were only 3000/week? That is unacceptable for investors. The fix: the sell side and shareholders should demand better disclosure. Vote with your feet.

3. Restaurant IPO valuations need a reality check. First year restaurant IPO valuation ratings need an asterisk. There is nothing fundamentally wrong with Noodles (NASDAQ:NDLS) other than their unsustainable claim to get to 2000 US units. It's a nice, differentiated concept. They will grow but not at Chipotle (NYSE:CMG) rates. Potbelly (NASDAQ:PBPB), El Pollo Loco (NASDAQ:LOCO) and Papa Murphy's (NASDAQ:FRSH) may grow if they can grow profitability beyond their geographical base. The Chipotle of 2015 is not the Chipotle of 2006. It can't be: The US is proportionately more overloaded with more restaurants during the Noodles 2013 IPO than CMG's 2006 IPO.

First year restaurant IPO price earnings ratios and Enterprise Value to EBITDA ratios need an asterisk because they may well fall later and resume upward momentum later after the post IPO equilibrium is found and real earnings and free cash flow growth is achieved.

Why does this matter? Growing restaurant brands that are over pressured by high valuations do stupid things. Good brands need to be given a chance to grow solidly.

4. Franchise overfishing, resulting subpar restaurant cash flows in the US: earlier in 2014, when fears of US restaurant wage increases were at its peak, several industry studies noted how low restaurant franchise EBITDA flow really was: 10 to 11%. The SS&G (now BDO) restaurant data survey in December just backed that up. For investors, franchisors, franchisees and anyone else: 11% EBITDA on a $1 million AUV base isn't high enough level to service debt, cover overhead and provide funds for maintenance and remodeling capital expenditures in the amounts needed.

The US is overfished, with too many franchise restaurants. One million restaurants in the US! Until the supply issue is addressed, franchise restaurants will chase the temporary +1 or +2 same store sales customer flow that migrates from one brand to another.

Franchisors need to take responsibility for their brand's future evolution. That they don't fully can be seen in the minimum wage debate. Franchisors, notably McDonald's, Burger King/Tim Horton's and Wendy's indicated that it was their franchisees that set the wages. While technically true, it is the franchisor that is the steward of the brand. If the wage goes to $20/hour, it is the responsibility of the franchisor brand to regenerate a store level model that works.

A place to start is to rightsize store physical plants smaller to get the CAPEX lower and to find ways to thin the system of weaker operators who want or need to exit. Closely associated with this is issue poor franchisor earnings disclosure: Sell side analysts covering Dine Equity have given up asking for meaningful information about the 100% franchised brands, and we noted one intrepid sell side analyst who was a journalist earlier could not pry the Burger King international new Russia and China sales levels. This was a pillar of their stated growth strategy and a metric that should be disclosed.

5. Restaurant free cash flow matters. For a client recently, I composed a 45 year snapshot of how sales components and building size has changed over the years. Guess what: while customer traffic (transactions) has declined, the building size has not come down.

The perception gap between the signal of the profit/loss statement and the other costs, and outlays that determines free cash flow is a material problem for an industry so CAPEX heavy. This same concern applies to the "asset light" franchisors, whose franchisees are the investors and have to make a return to be viable. This is not so complicated; performance appraisal systems at any level could be rejiggered to include CAPEX. You manage what you measure.

In the franchise finance world, the most discussed number is the EBITDA--EBBADABADOO as some call it. EBITDA is earnings before interest, taxes, depreciation and amortization. It is really a sub-total to the income statement. It is earnings without any charges for cost of funds, taxes or capital spending.

EBITDA's use began popularized as a credit metric, used in the 1980s M&A and credit analysis world--to test for adequacy of debt coverage. EBITDA is often the common denominator to track and report company buyout values: the acquisition enterprise value to EBITDA ratio is a very commonly reported metric. So much so that that's where the focus goes. And its use as a simple business valuation tool: the company is worth some multiple of EBITDA; the higher the multiple, the higher the price, and vice versa.

In the franchising space, where franchisors might report a simple EBITDA payback for an investment, or report EBITDA value in their franchise disclosure document item 19 section. The special problem there is this EBITDA is stated in terms of the restaurant level profit only--before overhead. Really, the problem is this: EBITDA doesn't show the whole picture. It is a sub-total. It doesn't show full costing.

EBITDA alone as the metric misses at least eight costs and expenses, that are vital to know, calculate and consider in operating and valuing the business as a cash and value producer. Using a business segment such as a store, restaurant or hotel as an example, here are the eight required reductions to EBITDA that must be subtracted, listed in order of magnitude of the cash outlay, to really get to operating economic profit.

Interest expense: the cost of the debt must be calculated. Interest is amount borrowed times the interest rate times the number of years. One can have rising EBITDA but still go broke.

Principal repayment: the business cash flow itself should contribute to the ability to pay back the principal debt. That often is in a 5 or 7 year maturity note and is another very large cost that must be considered.

Future year's major renovation/remodeling: once the storefront is built, it has to be renewed and refreshed in a regular cycle, often every 5-10 years, via capital expenditures (CAPEX). That often is 10-30% of the total initial investment, or more, over time.

Taxes, both state and federal: Financial analysis often is done on a pre-tax basis as there are so many complicating factors. But the reality is the marginal tax rate is about 40%.

New technology and business mandates: aside from the existing storefront that must be maintained, new technology, and new business innovation CAPEX must be funded to remain competitive. Example: new POS systems for restaurants, new technology for hotels.

Overhead: if the EBITDA value is stated in terms of a business sub-component, like a store, or restaurant or hotel, some level of overhead contribution must be covered by the EBITDA actually generated. Generally, there are no cash registers in the back office, and it is a cost center.

Maintenance CAPEX: for customer facing businesses (retailers, restaurants, hotels, especially) some renovation of the customer and storefronts must occur every year and does not appear in the EBITDA calculations. New carpets, broken windows, you get the idea. In the restaurant space, a good number might be 2% of sales.

And finally, new expansion must be covered by the EBITDA generation, to some level. New store development is often a requirement in franchise agreements, and new market development necessary. While new funds can be borrowed or inserted, the existing business must generate some new money for the expansion.

You might say...these other costs and expenses are common sense, they should show up in the detailed cash flow models that should be constructed. Or they can be pro-rata allocated. But how times does this really happen? The EBITDA metric becomes like the book title....or the bumper sticker that gets placed on the car. You really do have to read further or look under the hood. And the saying is true...whatever you think you see in EBITDA...you need more.

Two weeks ago, McDonald's (MCD) announced it planned to refranchise up to 1500 units out of Europe and Asia Pacific, and announced a series of increased dividends and share buy back plans. In 2013, Wendy's (WEN) announced refranchising of 450 units in its non core markets.

In 2012, Burger King (BKW) and Jack in the Box (JACK) kicked into serious refranchising, so much so that Burger King (BKW) now only owns and operates the 52 units in Miami out of a 13,667 worldwide unit total.

Even Starbucks (SBUX) is finally franchising its flagship Starbucks brand, refranchising units in the UK and Ireland. YUM has been furiously refranchising since the mid 2000s but intends to keep China Company operated.

Franchising has a high percentage margin--McDonald's has an 83% worldwide franchisee operations margin, and is among the highest. YUM's David Novak seems to confirm that when he says "we love franchising--it's the highest possible margin business we can be in. "

The debate in restaurant circles about the proper mix of company and franchised units has been legendary. In the 1970s and 1980s, the trend was towards company owned locations. In the 1990s, as return on invested capital (ROIC) and awareness of free cash flow--profit less capital expenditures-- expanded, refranchising picked up.

See GE Capital's presentation slide below, from a presentation Managing Director Todd Jones gave last week, which has some telling comments on this topic:

Refranchsing means the company thinks it can make more on the royalties, and on rent surcharges (if it owns the real estate) and by reducing G&A and capital expenditures (CAPEX), versus operating the unit.

In my view, most times, refranchising involves weaker profit stores, lower than a magic profitability toggle point and typically involves weaker brands or weaker geographies in a brand.

Therefore, investors may like it, especially in the short term. But who is it good for?

Benefits of refranchising

Refranchising can be a stock catalyst, that is, it is some corporate new news, particularly if it funds increased dividends or buybacks, or if it is associated with more debt that can fund dividends or buybacks, that juices the stock. That what McDonalds is doing.

Optical improvement of the numbers: refranchising takes the lower units out of the base, and optically makes restaurant sales and margins improve, as both Wendy's and Jack in the Box have noted.

Refranchising should lower debt, to allow for special dividends or to improve credit ratings, to ultimately lower interest expense.

Wall Street hopes refranchising will smooth out earnings variability and will shelter the franchisor from food cost and labor inflationary forces.

Boost Return on Invested Capital (ROIC) metric: with unit sale proceeds and capital investment falling lower or to near zero, it provides a bump to ROIC, at least in the short term.

It can help out franchisees, as large franchisees have a need to get larger. This was the case in the 2013 Wendy's refranchising.

And, in some cases, if the company can't operate stores well, refranchising is a type of outsourcing of the problems, to others. Both YUM (KFC) and Burger King (BKW) have admitted franchisees operate more efficiently.

Limitations with refranchising

Over time, the ultimate risk is the company becomes an outsourced restaurant provider--no expertise in running restaurants.

Adaptability/flexibility hampered: franchised concepts take longer to get new products to market and keep the physical plant remodeled and renewed. In the US, Starbucks will always have an advantage over McDonalds as it can make decisions and implement market change quickly, while in McDonalds case it takes years to attain buy in and effect market change.

Franchisees live a narrower existence. They do have to pay a royalty and are generally territory constrained. In addition, the availability of funds and cost of debt for franchisees typically are unfavorable versus that of the franchisor. This implies higher cost of debt and missed opportunities. Franchisees have higher debt to EBITDA ratios. For example, the McDonalds 2013 US franchisees debt /EBITDA ratio is app. 5.4 times, versus about 1.4 times at MCD corporate. Higher debt=higher risk=higher cost.

As the franchised ratio increases, investors get less visibility. Restaurant franchisors universally avoid talking franchisee performance. Currently, Popeye's (PLKI) is the only publicly traded chain restaurant franchisor reporting its franchisee's profits quarterly--a EBITDAR number, which isn't perfect, but that is something.

Decreased company structure. Good franchisors run their company units as a training and development ground for franchisees. If the company store base is deteriorated or nonexistent, quality development staffing comes at risk.

Once the refranchising is done, that arrow is no longer in the quiver. What next?

The Bottom Line

Business is business. Every number and signal needs to be scrutinized. Refranchising is both a bullish and bearish indicator at the same time. It is not a panacea.

Ironically, in reaction to the McDonald's plans last week, Wall Street was not happy. They hoped for more catalysts to juice the stock higher.

Kudos once again go to Popeye's Louisiana Kitchen Inc. (PLKI) not only for a good Quarter One 2014 earnings results reported just last evening, but also for continuing the practice of being the only publicly traded restaurant franchisor that I'm aware of that reports its franchisees cash flow proxy number.

Popeye's reports franchisee EBITDAR--earnings before interest, taxes, depreciation and rent.

It's only a semi useful metric, as it misses rent and related expense, but also debt service and capital expenditures (CAPEX). Depreciation expense is an inperfect proxy for CAPEX.

In the first quarter of 2014, Popeyes franchisee community had an EBITDAR of 21.3%, compared to a 20.1% for the prior year. Franchisee same store sales were up 4.3%. Many more costs and expenses need to be subtracted to arrive at franchisee real economic gain, but at least it is some number.

Popeye's EBITDAR number is about 3.7% percentage points better than the GE Capital QSR survey sample published earlier this spring. Of course, you have to look at both dollars and percentages, per store to analyze fully.

Other franchisors do not want to talk about franchisee numbers. They don't have them, or the numbers are not good. Sometimes, franchisors are afraid and don't want to know them. But in any case, they should have them or should care.

Compare the Popeye's treatment to that of an article published by The Street's Laurie Kulikowski last week timed for Small Business Week.

Activists shouldn't have been surprised by the Red Lobster sale to private equity.

Darden missed opportunities over time.

Some Red Lobster levers for improvement exist.

To any close observer of the ongoing Darden (DRI) conflict as it has unfolded with its opponent activists Barington, and Starboard since late 2013, a Red Lobster sale to private equity was not a shocking outcome.

Consider:

Private equity has dry powder--unallocated funds-- available that it must put to use to earn a fee. Golden Gate had owned three restaurant brands and continues to own one, California Pizza Kitchen.

Darden, which was in trouble since at least 2007 trying to hit a 15% EPS model with the mature Red Lobster and Olive Garden restaurant brands, bought a lot of restaurant concepts at high price in 2008-2013, and wound up with a lot of debt. As the rate of casual dining traffic decline fell after the Great Recession, (Darden noted the casual dining overall space traffic fell 18% versus the peak) and core earnings fell, it had both dividends and buyback demands going up at the same time. A true cash flow squeeze resulted.

Darden had remodeled the entire Red Lobster chain by 2013 and needed to get some money out of its investment. (Why it remodeled Red Lobster first versus Olive Garden is a fascinating question.)

Red Lobster had underlying real estate that could be levered to lower the effective Golden Gate purchase price.

The question, is what now to do with Red Lobster? What are the "Lobster Levers"?

On the positive side, the brand ratings are not weak. It ranks roughly in the middle of the pack via the 2014 Brand Keys Customer Loyalty index but near the top of the 2013 Q4 Goldman Sachs Brand Equity Survey. The downside is there are no other national seafood players to steal market share from. Bonefish (Bloomin Brands) (BLMN) is just growing and Joe's (Ignite Restaurant Group) (IRG) has built its own crab niche.

It's not going to work its way out of trouble with more $10 television advertising that it has been pounding way with this week. It's going to have rent to pay. Darden has noted Red Lobster's customer base indexes older and lower income than the most desirable casual dining peers; it's got 706 units in an overbuilt US restaurant space. Keeping the same units and doing the same thing won't solve anything.

But what it can do is the following:

Close some units. Now that it is private and protected from the intense investment community focus on every metric, it can examine its store base. Note that American Realty executed sale leasebacks on 500 of the 706 units. A number of units were excluded for a reason, some were leased, some undesirable to do so.

Red Lobster reached its unit count peak in the US in 1996, at 729 units. It then closed 75 stores over the next four years, to arrive at 654 units in 2000, to then slowly grow again until 2013. The natural US unit cap seems to be much smaller than 700. A privately held company can work this.

With a rather low 9% reported adjusted brand EBITDA, the law of large numbers is there must be a number of units that are in the lower profit quadrant that upon closure, could result in positive cannibalization, and will improve the overall brand average profile.

Test and rebrand. Maybe because it was part of the central heritage of Darden, other than remodeling or wood grilling, there has been no real new concept ideation for years. A self serve Red Lobster lunch platform and Red Lobster/Olive Garden combo stores were tested recently and were a total waste of time and money. Such poor quality tests are indicated of a big concept ideation problem. Too much seafood on the menu and a very low level of alcohol sales are indicative of the problems.

Work international. All of its peers are. Darden just began a brief foray into ex-Canada international and franchising in 2013. As late as 2013! Missing the international opportunity was a great strategic flaw. The US is filled up with restaurants. Can't Red Lobster work internationally, somewhere?

Work franchising, joint and limited partnerships. Darden's problems with franchising went all the way back to a failed franchised venture in the 1970s. Franchising is difficult, well funded and capitalized franchisees have to be found. Darden said they didn't have the expertise. But it can be found. A new management mindset embracing franchising has to be developed. It can work in casual/fine dining: Ruth Chris (RUTH) has had 50% of its stores franchised to solid players forever, and Cheesecake Factory (CAKE) is working franchising and joint venture partnerships to get its international growth jump started. The Cheesecake founder, restaurant operator, David Overton "got it", but not Darden.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Think beyond Darden's real estate to determine if long term value is present.

Both the activists and Darden provided incomplete analysis.

Restaurant level EBITDA is a poor metric; free cash flow metric is better.

Watching the ongoing war between the Barington and Starboard activists that have stalked the Darden (DRI) casual dining giant since late 2013 has been like watching a tennis game where the two players volley consistently in the air above each others heads. The value of Darden's real estate is the real objective and no one is making the points properly.

Imperative for Investors: Ask for more information. Think: do I want my bonus now or later? Does divesting real estate do anything to fix the fundamental issues at Darden? The real essence of the Darden real estate argument hasn't been laid out by either side well, and a lot of analytical foundation is missing. Look beyond the initial real estate splash to assess long term value.

Background: Darden Issues Over Time

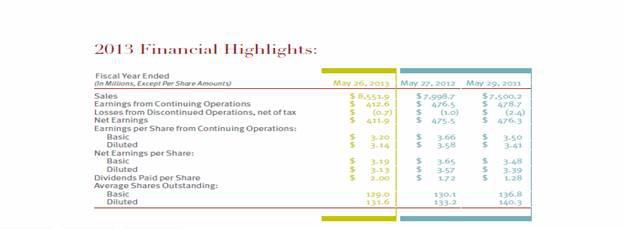

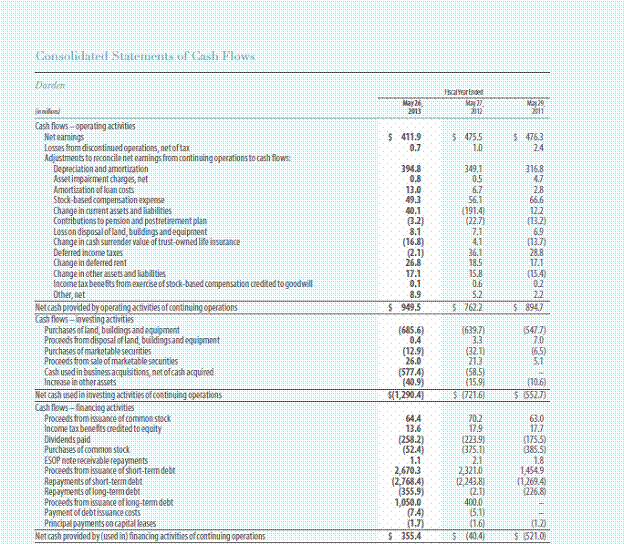

Darden owns and operates eight casual and upper end fine dining brands. For years it was on a strict 15-20% EPS target. It didn't franchise and until very recently was only US and Canada focused. As the US filled up with restaurants, and as casual dining sales growth began to slow down for many reasons in 2006-2007, it struggled to extract enough pennies and free cash flow to both remodel and execute buybacks and a rich dividend payout.

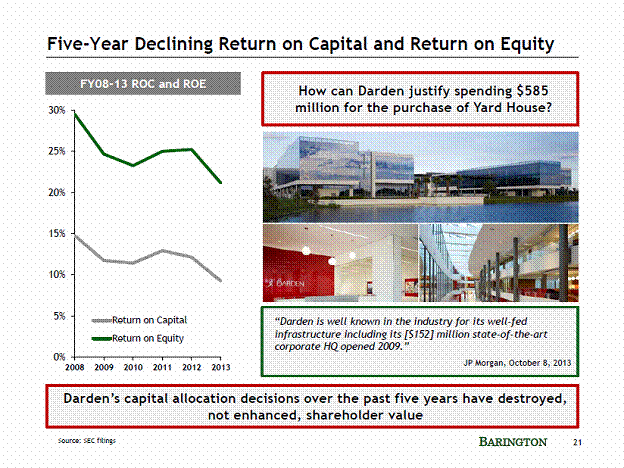

In 2008, Darden executed a $1.4 billion buyout of RARE Hospitality-the operator of Long Horn and Capitol Grill. Two other pricey buyouts occurred later, the small Eddie Vs seafood house in 2011 ($59M) and Yard House in 2012, the small but growing brew house ($585M). The buyouts as a group were costly, at well over 11X EBITDA, with Eddie V's almost 25X EBITDA. In each case Darden promised operating and G&A savings. The problem is, as the activists pointed out, the G&A savings didn't happen. DRI remained focused on the US and didn't even begin franchising or international until 2013 via tiny baby steps. Darden GAAP earnings and free cash flow dollars both were down per their 10K display:

Darden was sued in 2009 for a SEC 10b5 claim of unreasonable earnings claims coming from the RARE acquisition, but the Orlando Federal Court dismissed the action in 2009; given the high bar to securities litigation initial motions in the era after the 1995 Litigation Reform Act.

Full disclosure: I worked a special investigation of Darden's earnings projections after the RARE acquisition and didn't see how then how the acquisition synergies were "reasonable".

Guess what happened.

We are now where we are.

Darden faced the circumstances of slowing casual dining sales and traffic-which Darden itself did not create, but tolerated-- this weakness was apparent in 2007, before the Great Recession-but also having remodeled Red Lobster, now remodeling Olive Garden and putting a load on CAPEX, building very costly new restaurants--$5-6 million per box, pressure to increase dividends and buybacks...and covering the interest from the RARE, Eddie Vs and Yard House purchases. Check out the following Barington slide:

DRI's stock performance lagged in 2012 and 2013.

Barington pounced and was right on some of its calls in its introductory volley on December 17, 2013:

The Barington pitch was pretty logical until it got to two points:

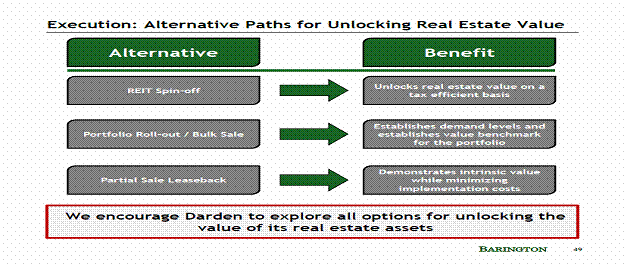

· Spin off the so called high growth brands-Capital Grill, Seasons 52, Bahama Breeze, Yard House, Eddie V-the entire DRI Specialty restaurant group, and

· Spin off the owned restaurant real estate into a REIT or sell the underling land.

While they weren't operators (Barington had some experience with the now fading Lone Star Steakhouse and the Pep Boys auto oil change chain as investor), they could read balance sheets and saw the company owned a lot of store real estate. Owning real estate was a restaurant financing and development strategy. In the early days it provided a veneer of security for the bankers but it also provided for a great mode of control: there were no landlords to hassle with, no step rent increases in the outyears or costly lease terminations should a site have to be closed. Working restaurant litigation matters as a one element of my consulting practice, I can testify that among the most common are real estate disputes.

Analytical Problems

In conference calls, Darden said that its Specialty Restaurant Group was profitable and could stand on its own. That was a bad admission, because almost certainly, that profit basis was an EBITDA value and not a free cash flow basis, which would have covered the CAPEX and debt service cost to build $5 million boxes. Restaurants don't highlight that metric.

Barington and Starboard have endlessly speculated on what a Darden REIT could trade for. Of course, there are no restaurant REITS to provide comparables.

See the following video from Howard Penny of Hedgeye, supporting Starboard and his super long call on Darden. Note that he touts the potential value of the REIT.

Starboard issued a 100 page "Darden Real Estate Primer". Despite all this, Barington and Starboard have failed to prepare analysis on the following key points:

1. What is the projected free cash flow profile for the outyears for a separated Olive garden/Red Lobster, and Specialty Restaurant Group?

2. What is a realistic REIT cash flow profile for some crappy real estate that Darden owns and needs to get out of? How much will Darden be liable in payments to the REIT?

It's not as simple as the Barington slide below, shows:

Restaurants and Real Estate

McDonald's (MCD) and Tim Horton's (THI) also are real estate centric, for the control and for the potential for real estate margin. Once the property is paid for, then it's practically a 100% profit flow through. As Jonathon Maze, Editor of the Restaurant Finance Monitor pointed out recently, "restaurant executives tend to take a longer view of real estate. It's a safety value; providing the company flexibility with options should things get bad."

The activists want short term gain, as does Wall Street generally. They tend to talk about "unlocking value". But over what time? Not many contemporary restaurant chains have such real estate intense balance sheets, as restaurant construction and land costs both rose in the 1990s-2000s.

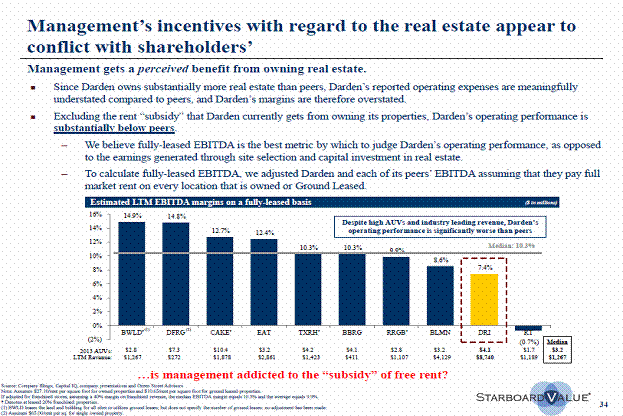

The implication in their pitch is that because the real estate is owned and because DRI does not pay cash rent, that it is somehow "sheltering" or incentivizing its RL and OG underperformance. From my long corporate staff experience, the corporate staff members who drive this-don't understand these intricacies at all. See the Starboard slide:

Memo to Starboard: any EBITDA metric is a very poor metric to judge performance.

Opinion:

So the real estate can be sold and proceeds generated to generate a big one time dividend, or a first time restaurant REIT will make big news splash. Good for 2015 or 2016 or when this is pulled off. But two questions are raised:

(1) Will the decoupling of the real estate fix the problems at Darden?

(2) What will you, Darden, do for me tomorrow?

The answer to Question One is almost certainly not. In fact, losing control of the real estate to either a REIT or a landlord owner should make it more difficult to reposition either Red Lobster or Olive Garden. Population and retail/restaurant trade patterns shift in the US, and there are too many casual dining restaurants now. That is one of Red Lobsters and Olive Garden's realities that Darden failed to address. While the land has value forever, many restaurant sites have an effective peak economic life of 20-25 years.

In terms of Question Two, it seems not clear. The activists have failed to lay out future year cash flows with and without real estate rents, and with and without portfolio breakage. They are talking the REIT valuation in one hundred page detail, however. Wrong entity to think about. Can Darden really close stores and not be stuck with big lease make whole payments? Darden hasn't laid it out clear case either.

If it's a church or a dollar store that comes in to backfill some closed Darden sites (two of Darden's closed sites in Indianapolis are that), think about being disappointed, either in the REIT, or decreased cash flow from Darden's core business.

On July 25, 2013, Starbucks (SBUX) delivered a Q3 double beat and stellar worldwide comparable sales (comps) of +8% (+9% in the U.S.)

Some analysts were concerned about the SBUX Q4 forecast of a mid-single digit comp. The high comps were said to be a kind of spike. SBUX explained that mid single-digit comps were likely in Q4.

CEO Howard Schultz explained that it would be irresponsible for SBUX to forecast high comps if it believed they were not attainable and that SBUX business trends were very solid.

He sharply concluded:

Now having said that, our expectations of ourselves that we are going to deliver a healthy comp growth in Q4 that our investors will be proud of. Let's get off the comp number, because it's not the issue, issue is we are building a great extraordinary endeavoring company and the comps are going to follow that.

Were the sell-side analysts right to be concerned about Starbucks' comp "slowing up?" See the below Starbucks comps chart.

My opinion: perhaps. Of course, the beginning of comps deceleration is an important investor signal and will first be seen on quarterly or monthly comps reporting. Only McDonald's (MCD) reports monthly comps.

But there are other more important questions.

In the retail and restaurant space, comp sales from year to year are given way too much emphasis in reporting and analysis. It becomes the headline bumper sticker. The metric, which strips out newly opened or closed stores that are "immature," is a proxy for business cadence and optempo momentum, and sometimes a proxy for profit flow through.

But the analytical problem is the year-to-year comp is only so meaningful. What happened last year - the base for the comp - could have been impacted by many factors such as weather, calendar shift, competitive and marketing calendar shifts and so forth. It's certainly possible to have a great 10-year, five-year or two-year comp trend, but to have a flat or modest current quarter comp calculation.

In the future, we urge investors of all sorts - and analysts - to ask more meaningful questions about the comp trend.

After getting the comp results, and a customer traffic and average ticket breakout, here are 10 more meaningful questions:

1. Did the comp achieved meet your internal budget?

2. What is the comp on a two-year basis, a five-year basis?

3. What tradeoffs to get this comp?

4. What's the comp on a rolling 12 month or rolling two-year basis?

5. How much profit flows through to the store level from this comp?

6. How much is the flow through on a percentage of incremental sales basis?

7. What is the standard, or theoretical profit flow through?

8. Is the incremental flow through attained via higher cost percentage leverage?

9. How much does incremental store level profit flow through to the corporate bottom line?

10. How does this comp affect variable compensation payout accruals?

One question to consider is whether this is a monthly period, or how many weeks were included in this comp and the prior period? The hugely symbolic and massive market cap McDonald's for instance, is still reporting on a traditional monthly basis, which makes for calendar noise, which we discussed previously on SA.

In the restaurant space, there is an inordinate amount of short-term action to maximize the comp.

Better investor and sell-side questions will enable the company to explain its rationale, and send truer & better picture to the market.

When you need an authority on understanding public franchisors, connect with me on LinkedIn - or just give me a call.

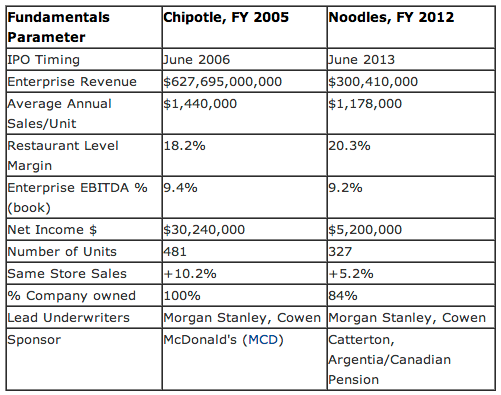

In one of the best IPO results of the year, the first restaurant IPO of the year, Noodles (NDLS) raised almost $100M and stock price more than doubled from its initial pricing at $18 to close at $36.75 on its first day. The Noodles CEO, Kevin Reddy, came from Chipotle (CMG), at an earlier stop in life.

Is Noodles the new Chipotle?

Chipotle IPO'd in June 2006. They are both fast casual concepts, Colorado based, both early movers. And there are many fundamentals comparisons. See the table below, prepared from both the Noodles and the Chipotle SEC S-1s, for their last full fiscal year before IPO, which shows the key fundamentals drivers:

Store economics look similar? Yes, in some ways:

· Fast casual operators, new buildings, new food types and popularized styles.

· Average Annual Restaurant Sales in the $1.2M to $1.4M range.

· Solid restaurant margins - Noodles now actually exceeded that of Chipotle in 2005 by 210 bpts.

· Totally or primarily company operated model.

Noodles' success demonstrates there is investor demand for new restaurant offerings and validates fast casual investor demand. I understand NDLS was twenty times oversubscribed. Catterton, Morgan Stanley and Cowen did a nice job.

The issue to keep in mind is the United States consumer space is not the same as it was in 2006.

Recession, fundamental changes in population, income, eating and dining preferences, commercial real estate site characteristics, and more U.S. restaurants in operation each year make for a more difficult 2013 and out conditions.

Noodles must deliver good quality, service, cleanliness and price/value, in a differentiated fashion, with good corporate stewardship and continue to build connections with guests, employees, investors and other stakeholders via its culture.

Mathematically, as it expands, it has to think a lot about occupancy costs. NDLS occupancy costs are now 9.9%. Chipotle's was 7.6% in 2005. Site supply is tight. Many legacy brands, the real first movers, like McDonald's and Dunkin' Brands (DNKN) got the early best U.S. sites.

Restaurants economics was built on 6-8% rent, but some restaurant operations are facing 15-20% rent for some sites. Too much push for too fast expansion will test the rent leverage especially for a $1.2 million sales concept.

The imputed IPO valuation from the NDLS IPO is already $800M, or an EV/EBITDA multiple of 26.6X. That's rich. But it's just the first day. I hope the pressure cooker investment world will take a break and give them a chance to grow smartly.

The restaurant space will be interesting in 2013. Sales issues, cost issues, expansion issues, franchisee issues. There are still too many restaurants in the US and x-US markets sales increases have slowed. The two industry leaders, McDonald's (MCD) and Darden (DRI), are both somewhat in the penalty box and under pressure. Here are our thoughts on 2013 issues and opportunities.

Comps Cliff Coming: In looking at 2013, it is likely restaurants will get off to a bad start. In Q4 and Q1 2013, the restaurant space will fall off a cliff of sorts: the comps bulge generated last winter. Driven then both by warmer weather, price increases, a bit lower sales of discounted items and the peak of the 2010-2011 restaurant recovery, the January-March 2012 number will be hard to beat.

The following chains will likely have the hardest sales comp comparisons in Q1. Every single chain had lower comps most recently reported than the Q1 peak, versus the most recent quarter or monthly update:

More sales news. Traffic throughout the sector has eroded since fall 2012. In the QSR space generally, traffic now is very marginally positive and average check is 2-3% favorable, but in the overall casual dining space, traffic is negative and totally offsets about a 2.5% check increase. A few positive standouts exist, however: Texas Roadhous ,Panera, Starbucks (SBUX) and Popeye's (AFCE).

One question is why was investor disclose so poor at YUM? The China same store sales trend is so stunningly negative - large sequential decreases from +19% in FY-11 to -6% just noted this week for Q4 2012, perhaps the largest decline anywhere over such a short time.

Extreme discounting is the newest news but is really an old story. The current price spectrum of restaurant TV ads runs from $.99 grillers at Taco Bell to $11.99 thirty piece shrimp at Red Lobster. This does not portend positive for the average check. The comps cliff has affected marketing strategies everywhere via low price marketing.

Earnings standouts: Texas Roadhouse, Panera, Starbucks and Popeye's were Q3 (and Q2) positive standouts: positive sales and traffic, sales and earnings beat $.01 or more over estimate. Does prior performance guarantee future results?

Dividends are the goal. Dividends will be important in a low growth, low return world. The US restaurant market is way overdeveloped and worldwide development takes time and proper store level economics. We will be glad to see companies like Dunkin Brands (DNKN,1.80% yield), Burger King (BKW,.90% yield), and Blooming Brands (BLMN, zero yield) finally work their way out of private equity positions so that more substantial dividends can be paid. THI, another pure play 100% "capital light" franchisor, is also low at 1.70%. That there are two coffee sector players in this group is interesting. Lower coffee commodity costs advantage will accrue to the franchisees, not the corporate entities.

Some IPOs and M&A will happen. We still wonder when Noodles will be ready for its IPO. Fast casual is "hot." Another fast casual brand, Pei Wei, could be a candidate once its lower newer unit open sales problem is fixed. Jamba (JMBA) seems to be of value for those strategic buyers who need an established beverage platform.

It was clear from the 2012 SBUX and DRI transactions that the path to a rich M&A valuation is to develop a unique but mainstream product that well-heeled restaurant majors can buy for entry at rich multiples. There will be continued private equity churn, they always have fresh powder to deploy. The wave of 2006-2008 PE acquisitions will soon come due to sell.

Several Turn Arounds should be watched. Interesting that the two worldwide restaurant leaders, MCD and DRI, are both challenged. No surprise that MCD went into a new product new news tempo decline as it changed CEOs in 2012. New products news yields sales.

It will be fascinating to watch Darden work out of its current tight cash position caused by lagging big brands and resulting profit shortfall, big remodeling capital expenditure (CAPEX) requirements and now debt service for its 2012 acquisitions. Of necessity, they will look for another acquisition in 2014, once its free cash flow position improves. We wonder if BKW has the worldwide AUV sales base potential anywhere except Latin America for franchisees to expand profitably.

Restaurants must more creatively test revenue and expense solutions: Restaurants can offset negative cost pressure and difficult comps pressure by looking at revenue increases beyond price increases and cost reductions beyond food portion cuts and labor hour savings. Unique store level pricing tiers and dual wage tiers to offset Obamacare are but two examples. The industry needs to test aggressively new ideas.

Defrancising v. Refranchising company strategy divergence will continue. Those who can operate restaurants well will continue to do so, those who cannot will refranchise. Panera, Texas Roadhouse and Qdoba are building new units, converting franchisees to company operation.

Franchisors still need to improve investor reporting and franchisee disclosure if they hope the franchising "capital light" business model will be sustained. How can DineEquity (DIN), now 100% franchised, be properly analyzed if there is no franchisee profitability reporting?

Is there room for optimism? Yes. Commodity cost forecasts have come in at the low end of forecasts. Some restaurants, such as Sonic (SONC), have finally sorted out their marketing focus.

Investor Recommendations. Look for a rough first half. Be ready for and go light or short the nine companies noted above that will have a negative same store sales cliff In Q1. Restaurant space investor attractiveness will be better second half 2013. Look for potential dividend upside effects at BKW, BLMN and DNKN late in 2013. DRI likely must cut its dividend so react light/short accordingly.

In watching the Q2 2012 restaurant space earnings, six brands interested us by exhibiting what we define as standout operating tempo-what we term OPTEMPO.

These six posted not only significant EPS beats of $.02 or more (meets or a penny over doesn't excite us much), but also positive traffic and positive early peek Q3 trends-that early Q3 trend prerelease info that some companies give. This quarter's entire group has performed well recently: Brinker (EAT),Texas Roadhouse (TXRH), Ruth Chris (RUTH), Popeye's (AFCE), Panera (PNRA), Papa John's (PZZA)

Common Denominators: Two casual dining operators, one fine dine operator, one bakery/café, one QSR pizza, one Chicken QSR operator were the group. Two of the six are steak centric (RUTH, TXRH), with one other making inroads into higher steak menu mix . Brand focus matters: four of the six were single concept restaurant operators, and two with two brands under the holding company structure (EAT, RUTH). There, one brand greatly predominates over the other (EAT: Chill's versus Maggiano's) and RUTH (Ruth Chris versus Mitchell's).

Steak centric: we noted in 2011 that steak centric operators did well, no doubt by the improving travel/expense account traffic. RUTH's peer, Del Frisco (DFRG) via its first call since its IPO noted positive same store sales (SSS)of plus 5.1% and traffic of +2.2% at the flagship Double Eagle units.

Positive traffic and early peek looks: All had positive traffic-RUTH greatest at +3.9%; AFCE and PZZA don't reveal traffic/check but one can deduce from the magnitude of the numbers it was positive).

All had consensus earnings move up $.02 or more over the last 90 days-PNRA highest at +$.11, PZZA +$.09, EAT +$.07. Three of the six had 5 analysts or less providing estimates, with PNRA, TXRH and EAT well in double digit analyst coverage territory.

None of these chains had eyeball high debt. Interestingly, none of the chains was actively refranchising, all were growing company units, with even franchisee heavy AFCE planning a significant slug of new company units.

Four of the six chains (RUTH, AFCE, PNRA, PZZA) had positive free cash flow increases from quarter to quarter. EAT and TXRH free cash flow was off from prior year but EAT is doing heavy duty remodels (and is still a huge cash generator) and TXRH is building new units.

Price/earnings ratios: only RUTH cheap but…

This group of restaurants, other than RUTH are not cheap. PNRA is the most expensive, but EAT and TXRH aren't nosebleed high valuation yet.

Friendly Ice Cream Corp. last week became the latest in a string of classic American restaurant chains to file for bankruptcy protection. The Wilbraham company, founded in 1935 , abruptly closed more than 60 locations and now hopes to reinvent itself as a leaner, more viable business by early December.

The road from private to public company started in 1978. "The Hershey Foods Corp. offered $162 million, or $23 a share, for Friendly Ice Cream's 7.05 million outstanding shares in December 1978. Friendly's board of directors, including chairman Prestley Blake, unanimously agreed to recommend the Pennsylvania company's offer to shareholders."

But the company only started franchising in 1997, or thereabouts.

However, about 25% of the locations were closed by mid 2000, and " Prestley Blake became increasingly critical of Friendly's upper management. In December 2000, he bought 892,000 shares of Friendly's stock for close to $2.5 million, making him its largest shareholder with a 12 percent stake in the company."

Sun Capital bought Real Mex from Bruckmann Rosser in, I believe 2006, and then the chain basically went bankrupt, KKR provided financing to keep it going, Sun gained possession again, and now it has collapsed under Sun for the second time in five years.

Why did this happen?

Sun, immediately after buying the chain, separated its real estate, selling its headquarters and the land under 160 of its 512 restaurants for more than $40 million. Sun used the money to fund its buyout of Friendly's, so that it payed little money down in the leveraged buyout.

Friendly's restaurants started paying higher rent.

When filing for bankruptcy, Friendly's, without referencing how Sun split its assets, cited high rents as one of the problems.

Sun restaurant chain Real Mex in the last few weeks also filed for bankruptcy.

Sun Capital bought Real Mex from Bruckmann Rosser in, I believe in 2006, and then after the chain basically went bankrupt, KKR provided financing to keep it going, and Sun gained possession again, and now it has collapsed under Sun for the second time in five years.

As in Friendly's, Sun put pressure on Real Mex by cheapening the product, for example, by putting less chicken in fajitas, a source said.

By starving its restaurants during a recession, Sun could not save enough costs to compensate for the traffic both Friendly's and Real Mex lost.

Private Equity Firms and Restaurants: Motivations, Track Record

Recently, the press has been full of reports of private equity (PE) firms receiving outsized returns on prior restaurant investments. Examples include the reported Sun Capital 13 times return on its 2003 Bruegger's investment, Olympus' Partners reported 8 times return on its K-Mac predominantly Taco Bell franchisee group, Falfurrias selling Bojangles (unit counts up 30% since 2007). CKE Restaurant's is now working a dividend via new debt for its owners, as did Dunkin Brands in late 2010.

We are maintaining a log and count so far 62 separate and distinct chain restaurant brands owned by PE firms, from large to small. That count will soon equal the number of publicly traded restaurants. And three big chains, Arby's, Long John Silver's and A&W were put out for sale in January 2011, and could join the PE ranks.

PE Economic Motives: The age-old laws of economics and investing hold here: buy low, sell high. Take money out of the business when you can. Lever up, pay debt down, then lever up again. Try to make improvements in the business. Hold for a 4-7 year timeframe. Think exit strategy from the beginning. Use OPM (other people's money) if at all possible, hold your cash equity infusion as low as possible so long as the debt isn't too high.

PE firms hope to deliver a 25 % plus annual compounded return on capital invested.

The spate of 2010 and 2011 restaurant activity has to do with (1) a general reopening of lending after the 2008-2009 recession, (2) lower corporate debt rates, and (3) PE firms with funds that must be put to use. Larger cash on cash percentage returns seem possible for "older" deals, when the required equity infusion was lower, at 20-30%, versus now. But the returns depend and will change over time.

The private equity firm promotes operational improvement, and synergiesvia a "buy to sell" mentality to get their investment back and realize a trading profit. With a 4 to 7 year term focus, they utilize both operational value creation and leverage and financial engineering. The balance depends on the PE firm's own expertise and focus. PE firm ownership doesn't guarantee success, however.

Highly franchised businesses, especially national brands, command a valuation premium since the earnings is thought to be more predictable and there is less (but not no) capital expenditures associated with a franchised system. Multi-unit franchisees are valued a bit less as they have a smaller development universe typically.

Is this bad or good for the brands? We don't know yet. Not much data is available.

In 2010, we looked at 2003-2007 era private equity deals that failed. Since data for privately held restaurants aren't much accessible, we defined failure to be either Chapter 11 or 7 filing or where unit counts declined. About 30% seemed successful, 40% in some mid-state or not determinable yet and about 30% had failed.

Interestingly, the success factor seemed to vary based on the brand strength, and position in the marketplace. The purchase price multiple, a proxy for debt, didn't seem to be greatly associated with the success or failure.

What about the franchisees?

In all of these chains, franchisees do all the customer execution work; bear the expense of the initial investment, ongoing capital expenditures and new unit expansion. They pay the royalties, and borrow the bulk of the funds needed for expansion. They are highly affected by credit market conditions.

Franchisees want buy in, dedication, and culture, since they have bought in, often for life. PE firms might be smart to leave competent management in place that can further build the culture and promote franchisor- franchisee coordination and unified accountability.

In relating to the PE firms, franchisees must realize that the PE firm is using both "trader skills" via a so called "buy to sell" mentality as well as business management skills to get a good return. They certainly want to make the business better. But each PE firm is different and has different motives and capabilities.

Franchisees should figure that businesses would be held for some time to recover investments but trader, market conditions would rule the timing. The exit plan might not be re-entry to the public markets, but might be sale to another PE firm. As other PE firms raise money, they need to put the funds to work, too.

For the 5 Most Fascinating Stories in Franchising, a weekly report, click here & sign up.

YUM Brands reveals its Quarter Three earnings tonight, with the earnings call tomorrow, October 6 2010.

The Wall Street Journal noted today the fact that YUM may hit the symbolic benchmark of 50% of earnings generated outside of the United States, either this quarter or next.

Their international focus is great and smart; YUM certainly looks smart developing and working its success in the China Market over the last decade. As we know, developing nations will have higher population and likely economic growth than the US/ Europe.

Yum Brands also is right at the 80% franchised units world-wide threshold, too.

KFC and Pizza Hut struggled greatly in the US since 2008, although they will say the Pizza Hut $10/any/any focus and its menu reengineering helps its sales trend. Since 2006, YUM has resisted per brand sales and margin breakouts, preferring instead to show combined world sector sales and margin trends.

We urge YUM and the security analysts that cover it to disclose and ask for per brand, US and outside of US franchisee and franchisor sales and restaurant margin data for both company and franchisee owned operations.

It's material enough of an issue, with 80% of the units franchisee operated, and will enhance worldwide decision making and analysis. YUM is a very complicated worldwide company.

Since February, 2010, there has been a spate of chain

restaurant merger and acquisition action underway: CKR (Carl's/Hardees's), Papa

Murphy's,Rubio's , On the Border, Lubys

buying Fuddruckers, just announced today, via Chapter 11 auction

results, for $60M); and rumored , Nelson Peltz selling Wendy's/Arby's. Some of the prices paid have been pretty low

(CKR) and some much higher.

This was all somewhat predictable. And all of these transactions involve franchisees, in the mix.

In some cases, private equity (PE) firms are eager to

rebalance their portfolios and sell their concepts outright, or to buy the

chains for later turnaround/later initial public offering (IPO). And Denny' recently had the battle royale of

proxy contests, where an outside, dissident force hoping to get board seats was

narrowly turned back.

How the debt is done, what the leverage and interest costs are

what the plans for management, supply chain and future business expansion matters to franchisees.

For most of these chains, about 80% of the stores are

franchised, and the franchisee owners

collectively have more money invested in the current total enterprise value

than does the company.

Just today, I saw a prominent restaurant security analyst's report

that valued franchise earnings (company franchise operational profit, the

royalty stream) at twice the multiplier rate of company owned stores...wow...that's

a lot of money for that fairly predictable piece of the top line that the

franchisor receives in royalties.

Of course, associations aren't consulted nor have much

information about this. The company views the buyout deal as complicated enough

without involving franchisees.

Here are some suggestions for franchise associations:

(1)Buy

some company stock. That elevates the franchisee associations a bit, and gives

access to stockholder meetings, and other communications.

(2)Monitor

the news, and include articles in your newsletters. Both the International Association

of Franchisees and Dealers www.franchise-info.ca and www.bluemaumau.org have daily news

clips and columns touching on these topics.

(3)Document

and come to agreement on your business strengths and weaknesses. And how to

respond. You may need this information someday.

John A. Gordon is a restaurant

financial analyst and management consultant, and can be reached via (619)

379-5561, or [email protected].

{kind=link}